You are currently viewing our boards as a guest which gives you limited access to view most discussions and access our other features. By joining our free community you will have access to post topics, communicate privately with other members (PM), respond to polls, upload content and access many other special features. Registration is fast, simple and absolutely free so please, join our community today!

The banners on the left side and below do not show for registered users!

If you have any problems with the registration process or your account login, please contact contact us.

Vancouver Off-Topic / Current EventsThe off-topic forum for Vancouver, funnies, non-auto centered discussions, WORK SAFE. While the rules are more relaxed here, there are still rules. Please refer to sticky thread in this forum.

I think Vancouver is heavily relied on real estate but it is not quite betting the farm on it. There are quite a lot of lucrative jobs.. (by that I say 80k for a BSc in Chem) Discovery Park(s) have tons of startups and keep expanding, there are a few large multinationals that anchors here eg Mckesson, MDA etc are always looking for EE. AVCorp is always looking for welders. Granted they are not cushy office work and often lab and STEM related, but they pay quite well for a job that only requires a bachelors. A lot of trades (carpenters, welders etc) move back and forth from the gas fields to town for projects already, so if RE going to tank in Vancouver, they are going to stay up North or in Ab for longer stints. They are short on housing up in that area anyways.

I think the problem with Vancouver is we have an over abudance of what Bill Maher called "Cave Drawers", who are hoping for the big break to be handed to them on a silver platter while working at service industries (restaurants, banks, etc etc). If a down turn makes some of them realise trades / making things are much better than selling credit cards in supermarket parking lots and gas statiions; I would say it is actually a good thing.

We tend to surround ourselves with people who are similar to us and put on our blinders to anyone else outside of our social circle. Most of the people in my social circle are yuppies and several make six figures (or close enough to six-figures), all are bright and innovative, some have equity, most socially adjusted and so on. However, this doesn't mean that the majority of people in Metro Vancouver are like this.

I think we can all agree that companies and organizations pay 10-20% lower in Vancouver than anywhere else in the country... and perhaps 40-50% less than American companies in the US. I think most people can accept a 20% gap in earning power to live in Vancouver: after all, our climate is good, the food is good, the air is clean - all things which help us live longer and more productive lives. However, when a yuppie couple (such as one you described) making a combined income of $150-200K cannot afford a detached home in a near suburb, such as Burnaby or Coquitlam, without significant financial help or better than average returns on their investments (in essence, luck), then there is an issue.

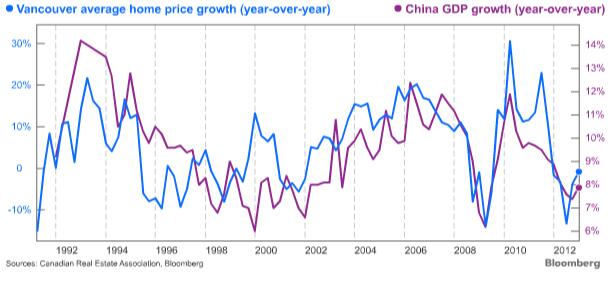

would be interesting to see other comparisons, though, i'm not sure that just because it looks pretty doesn't mean its significantly significant or that it is the only driver

would be interesting to see other comparisons, though, i'm not sure that just because it looks pretty doesn't mean its significantly significant or that it is the only driver

Absolutely.

Correlation does not imply direct causation.

I just found it to be an interesting graph. I can tell you right now that China's economy is not in a vacuum, and if they are doing well, then everyone else should be too and so on.

It is just one of those things that make you think.

OTTAWA - Canada's much-watched housing market is sending out mixed signals these days — even for analysts.

A spate of fresh data and yet one more market-cooling tweak from Ottawa last week has put one of the most important sectors in the Canadian economy, and the most important asset-source for most Canadians, on a kind of death watch.

That's because while some of the data, such as home prices and starts, is pointing to the soothing "soft landing" that homeowners, economists, banks and politicians are fingers-crossed hoping for, others, like land purchases and building permits suggest the real message is: the crash is coming.

Last week, Statistics Canada reported that building permits in the residential sector fell 12.9 per cent in June, and permits for multi-unit dwellings — mostly condos — sank even further by 18.8 per cent.

Even more frightening, research conducted by RealNet Canada found than in some of the bigger markets — Toronto, Vancouver and Calgary — residential land investments for future home building has already crashed through the floor, plunging 51, 52 and 30 per cent respectively.

Muddying the picture is that a new temperature reading of the housing market from the Canadian Real Estate Association (CREA) being released on Thursday is likely to show that home sales are doing just dandy and likely rose significantly in July, along with average home prices.

But David Madani of Capital Economics says it is the calm before the storm.

Or as he put it in a note to clients — "homebuilders are having a Wile E. Coyote moment" as when the perpetually ill-starred cartoon character realizes he has overshot the cliff and looks down to see nothing but air under his feet.

"It's astonishing to me that people are not picking up on this. If you see volumes crash and prices still rising, you shouldn't be thinking everything is fine, you should see that as a warning sign," he says.

"Here in Toronto, if you look at new home sales, we're at near-record lows. If you think about the implication this has for home building, new construction and all the jobs that go along with that, this is quite startling."

Some of that is yesterday's news.

Housing sales have recently begun trending upwards again — even in Toronto and Vancouver — after almost a year's slump brought on by Ottawa's decision to apply the brakes on mortgages last July.

Bank of Montreal chief economist Doug Porter predicts next week's report from CREA will show a 10 per cent surge in home sales from a year ago. He bases that on already reported data from big centres such as Toronto, Vancouver, Calgary and Edmonton, which all had boffo months, although there was a drawdown in Montreal and Ottawa.

Depending on whether you are an optimist or pessimist, this is either evidence of a soft or no landing, or a red flashing light.

The government's decision last week to put a limit on the issuing of mortgaged-backed securities is an indication that Ottawa views this development as anything but reassuring.

"Arguably this is the second last thing anyone wanted to see in the housing sector, a re-acceleration," Porter said. "That last thing people wanted to see was a hard landing."

Good news like strong home sales is potentially bad, says Porter, on the theory that Canadians are already drunk on housing, so imbibing more means the inevitable hangover will be all that much worse.

Benjamin Tal, CIBC's housing expert and deputy chief economist, wouldn't go as far as Madani in predicting a price correction of as much as 25 per cent, but he agrees the time has come for caution.

"If I was a speculator, I would not be buying," he says. "The days of flipping houses and speculating on increasing prices are clearly coming to a close. We are in the ninth inning of this boom."

It's been quite a ride. From January 2006 to June 2013, average home prices have risen from about $256,000 to almost $389,000, despite very low inflation and a little hiccup called the Great Recession. And, household debt from buying mortgages has ballooned to record levels above 160 per cent of disposable income.

The ride must end, agrees Tal, the only issue being is will it crash or simply coast.

So far, the consensus is on a slow coast, although the very real possibility of a hard crash has caused the Bank of Canada to put housing at the top of the list of domestic risks for the economy.

While housing constitutes only about seven per cent of the economy, the number underscores its impact.

Like a domino, if it topples, it triggers a chain reaction. Construction jobs are lost, household net worth diminishes, confidence drops and consumers start cutting back on other spending. On top of that, with families already highly indebted, defaults will almost certainly increase and lenders, such as banks, could find themselves taking enormous losses, dropping equity values, leading to tighter credit and slower growth. And on it goes in what economists call a re-inforcing negative feed-back loop.

"If we were indeed to have a serious setback in housing it would have pretty wide implications on the economy," says BMO's Porter.

The consensus view is s2till that the market will slowly decelerate rather than brake hard, if only because the economy continues to grow, employment is holding up and most critically with interest rates at super-low levels, borrowing is cheap.

But even Tal, who is in the soft-landing camp, acknowledges the danger. The housing market could stand to take a breather, he says.

That may be a good thing, given the exposure young people face in trying to buy even a starter home in cities like Toronto and Vancouver.

"I think the rental market will be stronger (going forward)," he predicts.

"We in Canada, especially in big cities, are fixated on buying a house the moment you graduate from university or get married. That's not the case in many other cities in the world, there young people don't think it a crime to rent for a time."

It’s getting hard to keep track of how many times the federal government has tried to lasso the galloping housing market.

The latest is a move by Canada Mortgage and Housing Corp., a federal Crown corporation, to limit the guarantees it offers banks on their mortgage-backed securities.

Lenders have enthusiastically tapped the generous guarantee to turn mortgages into near government-quality bonds.

MORE RELATED TO THIS STORY

Canada's housing market still running hot

GLOBE EDITORIAL Canada, the U.S. and the weaning of the mortgage markets

Housing starts soften, hinting at builder caution amid sales tumult

VIDEO

Video: Obama makes pitch for mortgage reform

A for sale sign is seen on the lawn of a Toronto home. The Canadian Real Estate Association says home sales were down in June from year-earlier levels, but higher compared with the previous month.

REAL ESTATE

Video: How home buyers will be affected by the new CMHC cooling measure

VIDEO

Video: NYC neighbourhood still in ruins post-Sandy

It has been a no-brainer for the banks. The program was so popular that lenders had used up nearly 80 per cent of this year’s available government guarantee by the end of July – even as the real estate market slowed.

But the episode highlights a troubling upshot of the real estate boom.

The federal government has had a major role in stoking the rapid expansion of mortgage credit in Canada. Now, as the long credit-fuelled rush into real estate appears to be stalling, taxpayers could be stuck with a large and unexpected bill.

Three-quarters of all Canadian mortgages are insured by the federal government, up from only 30 per cent in 1988. Ottawa guarantees a total of $900-billion worth of mortgage insurance.

It would take a spectacular crash for the government to have to pay out on all that insurance. But for a sense of scale, the $900-billion exposure dwarfs the federal government’s net debt of $676-billion.

It is now clear that Ottawa is not only worried about homeowners borrowing too much. The government is also concerned about its own exposure, and it’s scrambling to limit the potential risk to taxpayers.

The irony is that it is a problem almost entirely of the government’s own making. Starting in the late 1970s, successive Liberal and Conservative governments made it a national policy to aggressively encourage home ownership. The government offered mortgage insurance to all homeowners via CMHC, then it expanded those guarantees to private mortgage insurers.

In the 1990s, the minimum down payment on mortgages was dropped to 5 per cent from 10 per cent. In 2006, CMHC introduced a no-down-payment insurance product and it extended mortgage insurance to cottages and second homes.

Efforts gathered steam in the early 2000s, with the creation of government-backed mortgage bonds and the decision by CMHC to remove the $250,000 cap on the size of mortgage it would insure. Ottawa would eventually reimpose a cap of $1-million.

The government also lengthened the maximum amortization period for mortgages from 25 years to 30 years in 2005, to 35 years in 2006 and eventually 40 years (it has since been set back to 25 years).

The final incentive to expand the availability of mortgage credit was the insured mortgage purchase program, which enabled banks to sell their government-backed mortgage bonds back to CMHC at a profit.

All these programs were like rocket fuel for the real estate market in a low-rate environment. They triggered a rapid expansion of risk-free mortgage credit, and, arguably, drove the rapid runup in house prices in the past decade.

“The evidence is fairly telling,” analysts at corporate bond manager Canso Investment Counsel Ltd. of Richmond Hill, Ont., argued in a recent newsletter. “Housing became more expensive for Canadians because of the misguided efforts of the CMHC to make mortgages easier to obtain.”

Canso estimates that the combined impact of successive federal programs may have added as much as 50 per cent to house prices in key markets, such as Toronto. Canso estimates that the “affordable” price of an average two-storey home in upscale North Toronto is $615,000 – well shy of the actual price of $900,000.

As Canso bluntly puts it: “Canada borrowed its way out of the 2009 recession by stoking our residential housing market to absurd levels. We cannot afford the houses we are in.”

Ottawa is now wisely unwinding many of its pro-home-ownership policies.

It’s not yet clear if these efforts will produce a soft landing or a more disorderly unwinding, as some analysts fear.

Looking back, Finance Minister Jim Flaherty’s constant badgering of Canadians about excessive borrowing may have been a diversion.

He could have worried more, and sooner, about the government’s own behaviour in pumping up house prices.

The worst thing you can have is the government saying, "we're here to help!"

Thanks but no. Key line here: "As Canso bluntly puts it: “Canada borrowed its way out of the 2009 recession by stoking our residential housing market to absurd levels. We cannot afford the houses we are in.”

at the 13:00 minute market, is talking about loan forgiveness and keeping people in their homes, instead of the US style mass evictions.

**edit, they were talking about a slump in the end of last year, and how long it might last. Not long enough apparently, as of course, it went up again after that was shot.

Awesome. Those that didn't buy in, and stayed renting instead of buying get to subsidize those that did so they can keep their houses.

if you already purchased a home, and looking to upgrade to a bigger home, does market fluctuation really affect you?

assuming you're wanting to stay in a similar area, the fluctuation of the 'upgrade' home and your 'current' home would be relatively the same, so either way you're just be paying the differential on the 2 homes?

meaning if a $900k home drops in price say $100k, a current home worth $600k could drop $100k as well so i'd still be paying around $300k to 'upgrade'?

i know 1 type of home could depreciate/appreciate faster than the other...but am i over simplifying it?

if you already purchased a home, and looking to upgrade to a bigger home, does market fluctuation really affect you?

assuming you're wanting to stay in a similar area, the fluctuation of the 'upgrade' home and your 'current' home would be relatively the same, so either way you're just be paying the differential on the 2 homes?

meaning if a $900k home drops in price say $100k, a current home worth $600k could drop $100k as well so i'd still be paying around $300k to 'upgrade'?

i know 1 type of home could depreciate/appreciate faster than the other...but am i over simplifying it?

I imagine that the majority of first-time home owners in Vancouver have condos (or some other type of strata property) which will likely suffer decreases more acutely than detached homes. Posted via RS Mobile

if you already purchased a home, and looking to upgrade to a bigger home, does market fluctuation really affect you?

assuming you're wanting to stay in a similar area, the fluctuation of the 'upgrade' home and your 'current' home would be relatively the same, so either way you're just be paying the differential on the 2 homes?

meaning if a $900k home drops in price say $100k, a current home worth $600k could drop $100k as well so i'd still be paying around $300k to 'upgrade'?

i know 1 type of home could depreciate/appreciate faster than the other...but am i over simplifying it?

Absolutely...IF you have equity in the home.

Bought it for 400k 8-10 years ago, watched value rise to 600k, and fall back to 500k. Keeping the math simple, you put 10% down, so you went 40k equity to 240k equity down to 140k in equity, which then forms a downpayment of 15.5% of the 900k home(or 17.5% of the reduced price of 800k)

You're good. Buy away.

Bought your 600k house for 600k in 2007 at the peak of the market. Now want to sell. Your 10% down was 60k, house now worth 500k. Hell, once again, not doing math, let's say for fun that you paid down 10k in principal in the time you lived there(you didn't). 70k in equity. You are still upside down on the house, so you may want to upgrade your house, but you can't. Your equity is burned. Your mortgage is 530k, on a house worth 500k. And that's a 10% downpayment which NO one has. It's all done on 5%(for the most part).

You are not good, and you will not buy away.

A 16% drop in prices is rather severe on an economy, so the math won't come as a surprise to anyone in that situation at that point.

On a 5% drop, your mortgage is 530k, on a house worth 570k. Your new downpayment is less than your old downpayment and you want more house. You stretch to 5% downpayment to make it count for more house and become more susceptible to fluctuations in the price of homes.

So the netherlands have been seeing price drops recently. Over there they said that there was no bubble. Prices there have dropped 10% in a short amount of time, it will be interesting to see what happens in the next 6-10 months there, if prices will stay flat or start dropping more. The country also suffers from high debt to income ratio, similar to Canada.

The Netherlands - home to the most indebted households in the euro zone - is undergoing a severe housing correction which will further dampen consumer spending and extend the country's recession, according to Michael Taylor, an economist at Lombard Street Research.

"Going Dutch", a term used to indicate that each person pays for himself, may be associated with frugality. But recent data shows that households in the Netherlands have been anything but frugal.

The country has the highest total household debt-to-income for the seventeen countries that share the euro, according to Eurostat. At more than 250 percent, it far surpasses the same figure for Ireland, Spain and Portugal.

Surging house prices in the country have now given way to a "painful post-bubble adjustment", Taylor said, similar to the adjustments in Spain and Ireland.

Play Video

UK Housing: A Disaster Waiting to Happen?

Andy Brough, fund manager at Schroders, talks to CNBC about UK housing and how the idea of pouring more debt on people to buy an asset which looks overpriced is going to end in tears.

"The Dutch housing bubble was not caused in the main by inappropriately low interest rates following euro membership as occurred in Spain and Ireland. Instead generous tax relief on mortgages fueled a prolonged period of strong demand that pushed house prices to extreme levels," Taylor said in a research note on Monday.

"Any revival in external demand will almost certainly not be strong enough to lift the economy out of recession."

Home prices are nearly 10 percent cheaper in June than a year ago, Statistics Netherlands said on Monday. The price drop is more substantial than in the preceding month when house prices fell by 8.2 percent.

(Read More: UK house prices leap to record high)

This is particularly bad news for the short-term consumer outlook, Taylor said, adding that this deleveraging by the household sector will exert a strong downward influence on consumption and the wider economy.

The Netherlands economy has contracted in seven out of the last eight quarters and consumer spending has been in an almost continuous decline for two years now. Household spending on goods and services was down 1.8 percent in May 2013 from May 2012, according to the latest data from Statistics Netherlands, with spending on durable goods falling dramatically.

The chart above shows that declining consumer spending has been correlated with falling house prices in recent years.

But despite the data, yields on the country's benchmark 10 -year sovereign bonds remains below 2 percent and Netherlands still has a 'AAA' rating from Fitch, albeit with a negative outlook.

"The Netherlands is in the midst of a prolonged balance sheet recession. Output is likely to continue on a declining trend at least until house prices stabilize, but there is little prospect of this on a 12 to 18 month view," Taylor said.

(Read More: Dutch finance minister tanks markets; is cyprus a 'template' for Europe?)

"The advantage the Netherlands has over some other members of the euro zone is that it is well-placed to benefit from a recovery in external demand. Unfortunately any such revival will not be sufficiently strong to lift the economy out of recession. GDP (gross domestic product) is likely to contract by between 1 percent and 1.5 percent this year."

So the netherlands have been seeing price drops recently. Over there they said that there was no bubble. Prices there have dropped 10% in a short amount of time, it will be interesting to see what happens in the next 6-10 months there, if prices will stay flat or start dropping more. The country also suffers from high debt to income ratio, similar to Canada.

what's everyone's thoughts on a vancouver special, say built around 1980-ish vs current day cookie cutter houses? seems pricing is similar (depending on location) or the new(er) homes might be anywhere between $100-200k more.

given min. maintenance, the feeling i've always had is that quality of construction in those older homes were/are better than present day.

what's everyone's thoughts on a vancouver special, say built around 1980-ish vs current day cookie cutter houses? seems pricing is similar (depending on location) or the new(er) homes might be anywhere between $100-200k more.

given min. maintenance, the feeling i've always had is that quality of construction in those older homes were/are better than present day.

it's a house by house situation - a vancouver special could have been built to the highest quality, but if they had a small leak 15 years ago that was never fixed and as such part of the frame is rotting... well, you get the picture.

don't buy now. if you do, get a good inspection done - it can't tell you everything (i.e. whats behind the wall or under the carpet), but it can give you an indication of how good the house is. if you EVER buy without an inspection due to wanting to get a certain house, you deserve everything you will get, and you will get headaches...

i'd personally want a vancouver special, as it should, in theory, be on a bigger plot - i'd check the zoning to, in consideration for future refurbishment or development of that land. but we're talking when prices are 60% of what they are today. That day will come, we are stupid expensive right now, and rates are going up, these are two facts, based on sound criteria. We're not manhatten, hong kong, london, paris - we're vancouver, very little economy, and not much going on... we don't deserve these heightened prices.

I would agree that the 1980s were built better but you'll have to take in the fact that its 30+ years of wear and tear versus something built more recent with limited use. Really depends if the owners took care of the house

I would agree that the 1980s were built better but you'll have to take in the fact that its 30+ years of wear and tear versus something built more recent with limited use. Really depends if the owners took care of the house

also consider improvements in technology, unless updated, i'd imagine the new house will be more efficient (better insulation, more efficient heating, etc)

while these can be updated, things like corroded lines, poor electrical work, etc. costs a lot.

the only way i'd buy an older house would be to rip the interior apart and redo all those bits, but i'd be looking to enter at a much lower price than what we're at right now.

again, i'd say location and size of plot (and exposure to the sun, for weirdos like me that LOVE the sun) are the most important aspects in buying a house.

There are some good areas, and times and bad areas and times.

Not every house gets fully inspected for every permit. They can't hold you up for a month while they get to it. So if you have a large building boom, such as south of the fraser in the 80's, some things get over looked.

Hell, I've seen changes in a spread of 10 years in apartment buildings. They switched to flexible copper tubing, bent the hell out of it, and now it pinhole leaks like a sieve. Up the street, a building was built 5 years earlier and its tight. Go figure.

New tech can affect you too. No one can test this shit for 40 years to see the results of aging on a material...so they do what they can, release it and see how it goes.

Worked out great for the makers of Polybutylene Pipes.

4444 is right that this shit costs a fortune to re-do. That's why a lot of the shit houses get pulled as everyone wants a 12 bedroom house with a lawn that can be mowed with scissors. Personally, I like old houses, issues and all..but we're in the minority.

You are currently viewing our boards as a guest which gives you limited access to view most discussions and access our other features. By joining our free community you will have access to post topics, communicate privately with other members (PM), respond to polls, upload content and access many other special features. Registration is fast, simple and absolutely free so please, join our community today!

The banners on the left side and below do not show for registered users!

You are currently viewing our boards as a guest which gives you limited access to view most discussions and access our other features. By joining our free community you will have access to post topics, communicate privately with other members (PM), respond to polls, upload content and access many other special features. Registration is fast, simple and absolutely free so please, join our community today!

The banners on the left side and below do not show for registered users!